Accessing quality mental health care often depends on understanding how your insurance coverage works. In 2026, more Americans than ever recognize the importance of mental wellness, yet navigating health insurance for mental health remains complex. Federal regulations require equal treatment of mental health and physical health conditions, but knowing your specific benefits, limitations, and rights can make the difference between affordable care and overwhelming costs. Whether you need substance abuse assessments, court-mandated evaluations, or ongoing counseling services, understanding your insurance options empowers you to get the help you deserve.

Understanding Mental Health Parity Requirements

Federal law mandates that insurance companies treat mental health conditions with the same importance as physical health conditions. The Mental Health Parity and Addiction Equity Act established groundbreaking protections for individuals seeking behavioral health services.

What Parity Means for Your Coverage

Mental health parity ensures your insurance plan cannot impose stricter limitations on mental health benefits compared to medical or surgical benefits. This protection applies to several critical areas:

- Treatment limitations cannot be more restrictive for mental health services

- Financial requirements must match those for physical health care

- Out-of-pocket costs should align with medical services

- Prior authorization processes must be equivalent

Copayments, deductibles, and coinsurance for mental health services should mirror what you pay for a physical health visit. If your plan charges a twenty-dollar copay for a primary care visit, it cannot charge fifty dollars for a therapy session.

Coverage Scope Under Federal Law

Health insurance for mental health must include comprehensive services as essential health benefits. Plans sold through the Health Insurance Marketplace and most employer-sponsored insurance programs must cover behavioral health treatment, counseling, psychotherapy, and inpatient psychiatric care.

The National Alliance on Mental Illness explains mental health parity in practical terms that help consumers understand their rights. This coverage extends to substance use disorder treatment, crisis intervention services, and psychological evaluations including those required for immigration purposes or court proceedings.

Essential Mental Health Benefits in 2026

Modern health insurance plans recognize mental health as a cornerstone of overall wellness. HealthCare.gov outlines comprehensive mental health coverage requirements that insurance companies must follow.

Core Services Covered

Your health insurance plan should provide access to multiple types of mental health services:

- Outpatient counseling and therapy sessions with licensed professionals

- Inpatient psychiatric hospitalization for severe mental health crises

- Substance abuse assessments and treatment programs

- Medication management for psychiatric conditions

- Psychological testing and evaluations for diagnostic purposes

- Crisis intervention services including emergency mental health care

Many individuals require specialized evaluations such as assessments of suicidal behavior or comprehensive psychological testing. These services fall under essential health benefits when medically necessary.

Preventive Mental Health Services

Insurance plans increasingly cover preventive mental health screenings at no cost to patients. Annual depression screenings, anxiety assessments, and behavioral health check-ups help identify concerns before they escalate. Early intervention through these preventive services can reduce the need for intensive treatment later.

Specialized assessments like screening for cognitive decline may be covered as preventive care for certain age groups or risk categories. Always verify coverage details with your insurance provider before scheduling evaluations.

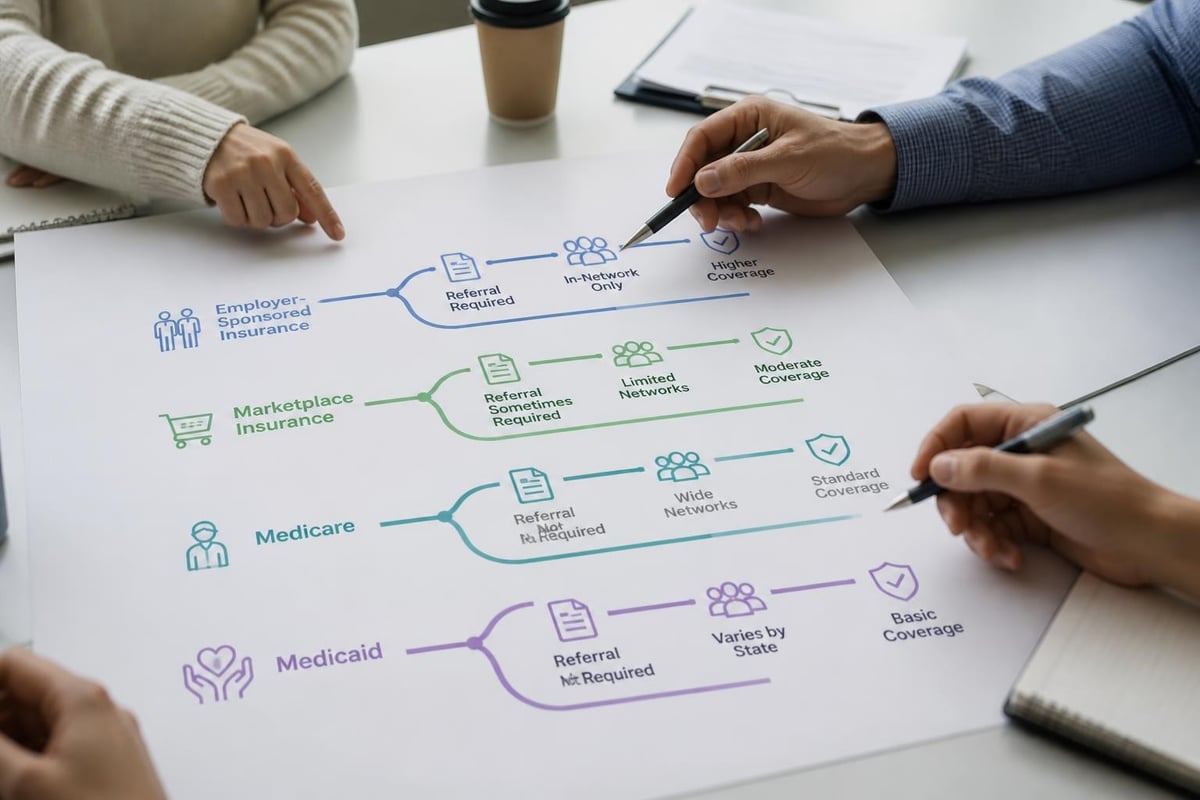

Types of Mental Health Insurance Plans

Different insurance structures provide varying levels of mental health coverage. Understanding your plan type helps you maximize benefits and minimize out-of-pocket expenses.

Employer-Sponsored Health Insurance

Most Americans receive health insurance for mental health through employer-sponsored group plans. These plans typically offer robust mental health benefits due to parity requirements and the Affordable Care Act provisions.

| Plan Feature | HMO | PPO | EPO | POS |

|---|---|---|---|---|

| Referral Required | Yes | No | No | Sometimes |

| Out-of-Network Coverage | Limited | Yes | No | Limited |

| Primary Care Physician | Required | Optional | Optional | Required |

| Mental Health Flexibility | Moderate | High | Moderate | Moderate |

Health Maintenance Organizations (HMOs) require referrals from your primary care physician before seeing a mental health specialist. Preferred Provider Organizations (PPOs) offer more flexibility to choose providers but may have higher premiums.

Marketplace and Individual Plans

Health insurance purchased through state or federal marketplaces must include mental health and substance use disorder services as essential health benefits. These plans follow strict parity guidelines regardless of metal tier (Bronze, Silver, Gold, Platinum).

Individual plans outside the marketplace may offer mental health coverage, but benefits vary significantly. Always review the Summary of Benefits and Coverage document before enrolling.

Medicare and Medicaid Programs

Medicare Part B covers outpatient mental health services including therapy and counseling. Part A covers inpatient psychiatric care. Medicare Advantage plans often provide additional mental health benefits beyond original Medicare.

Medicaid programs vary by state but generally provide comprehensive mental health coverage. Many states expanded Medicaid under the Affordable Care Act, improving access to behavioral health services for low-income individuals.

Navigating Coverage for Specialized Mental Health Services

Beyond standard therapy and counseling, many individuals need specialized mental health evaluations. Health insurance for mental health should cover medically necessary assessments, though authorization requirements vary.

Court-Mandated and Legal Evaluations

Psychological evaluations required by courts, attorneys, or legal proceedings present unique insurance challenges. Coverage depends on whether the evaluation serves a medical treatment purpose or purely legal function.

Treatment-focused evaluations that inform your ongoing care plan typically receive coverage. Pure forensic evaluations requested solely for legal proceedings may not qualify as covered services. Understanding this distinction prevents surprise bills.

When courts require assessments for substance abuse as part of treatment planning or rehabilitation programs, insurance companies often provide coverage. Documentation from legal representatives or treatment providers strengthens authorization requests.

Immigration-Related Psychological Evaluations

Individuals navigating immigration processes sometimes need comprehensive psychological evaluations. These assessments document mental health conditions, trauma histories, or hardship factors relevant to immigration cases.

Insurance coverage for immigration evaluations varies considerably. When the evaluation addresses diagnosed mental health conditions requiring treatment, insurers may provide partial or full coverage. Evaluations conducted purely for immigration documentation without treatment implications rarely receive coverage.

Advocacy and documentation from your mental health provider can improve coverage outcomes. Clear medical necessity statements explaining how the evaluation informs treatment planning increase approval likelihood.

Specialized Testing and Assessments

Comprehensive psychological testing including intelligence assessments, neuropsychological evaluations, and learning disability screenings may require prior authorization. Tests like the WAIS-IV Wechsler Adult Intelligence Scale or Wechsler Intelligence Scale for Children serve important diagnostic purposes.

- Obtain pre-authorization before scheduling comprehensive testing

- Request detailed coverage explanations for specific test batteries

- Document medical necessity through provider notes and referrals

- Appeal denials with supporting clinical documentation

- Explore payment plans for non-covered portions

Screening for learning disabilities and related assessments help children and adults access appropriate educational and workplace accommodations. Insurance coverage improves when evaluations directly inform treatment planning.

Managing Costs and Maximizing Benefits

Even with comprehensive insurance, mental health care involves out-of-pocket costs. Managing the high cost of mental health care requires strategic planning and understanding your benefits thoroughly.

Understanding Your Cost-Sharing Responsibilities

Health insurance for mental health involves several types of cost-sharing that affect your total expenses:

Deductibles represent the amount you pay before insurance coverage begins. High-deductible health plans may require significant upfront payments before mental health benefits activate. Copayments are fixed amounts paid at each visit, while coinsurance represents percentage-based cost-sharing after meeting your deductible.

Out-of-pocket maximums cap your annual spending on covered services. Once reached, your insurance pays one hundred percent of covered costs for the remainder of the plan year.

In-Network Versus Out-of-Network Providers

Choosing in-network mental health providers dramatically reduces costs. Insurance companies negotiate contracted rates with network providers, resulting in lower copayments and coinsurance for patients.

Out-of-network providers charge higher rates, and insurance companies reimburse smaller percentages. You pay the difference between the provider's charge and the insurance reimbursement. Some plans exclude out-of-network mental health coverage entirely.

| Cost Factor | In-Network | Out-of-Network |

|---|---|---|

| Copayment | Twenty to forty dollars | Not applicable |

| Coinsurance | Ten to twenty percent | Forty to fifty percent |

| Balance Billing | Not allowed | Often permitted |

| Claims Processing | Automated | Manual submission |

Balance billing occurs when out-of-network providers charge patients for amounts exceeding insurance reimbursement. In-network providers cannot balance bill beyond agreed cost-sharing amounts.

Prior Authorization and Medical Necessity

Insurance companies frequently require prior authorization for mental health services beyond basic outpatient therapy. Inpatient psychiatric care, intensive outpatient programs, and comprehensive psychological testing typically need pre-approval.

Your mental health provider submits clinical documentation demonstrating medical necessity. Insurance reviewers evaluate whether proposed treatment meets coverage criteria and follows evidence-based practice guidelines.

Denials happen even for clearly necessary services. Understanding your appeal rights and providing thorough clinical justification increases approval rates. Request detailed denial explanations and work with your provider to address specific insurer concerns.

Special Considerations for Substance Use Disorder Treatment

Health insurance for mental health explicitly includes substance use disorder treatment under federal parity laws. Coverage extends to detoxification, residential treatment, outpatient counseling, and medication-assisted treatment programs.

Levels of Substance Abuse Care

Insurance plans must cover medically necessary substance abuse treatment across intensity levels:

- Outpatient counseling for individuals maintaining daily functioning

- Intensive outpatient programs requiring multiple weekly sessions

- Partial hospitalization providing day treatment without overnight stays

- Residential treatment offering twenty-four-hour structured care

- Inpatient detoxification for medically supervised withdrawal management

Coverage decisions depend on clinical assessments determining appropriate care levels. Insurers cannot arbitrarily limit treatment duration or session frequency more restrictively than medical services.

Medication-Assisted Treatment Coverage

Evidence-based substance use disorder treatment often combines counseling with medications like buprenorphine, methadone, or naltrexone. Insurance plans must cover these medications without discriminatory prior authorization requirements.

Pharmacy benefits for substance use disorder medications should mirror coverage for other prescription drugs. Higher copayments or stricter quantity limits specifically targeting addiction medications may violate parity requirements.

Emerging Mental Health Coverage Trends in 2026

The mental health landscape continues evolving with new treatment modalities and service delivery methods. Health insurance for mental health adapts to cover innovative approaches demonstrating clinical effectiveness.

Telehealth Mental Health Services

Virtual mental health appointments became mainstream during the pandemic and remain widely covered in 2026. Most insurance plans reimburse telehealth therapy sessions at the same rate as in-person visits.

Technology platforms enable convenient access to licensed therapists regardless of geographic location. Rural residents and individuals with mobility challenges particularly benefit from telehealth mental health coverage.

Alternative and Complementary Treatments

Some insurance plans now cover evidence-based alternative treatments for mental health conditions. Transcranial Magnetic Stimulation (TMS) receives coverage for treatment-resistant depression when patients meet specific clinical criteria.

Other emerging treatments may have limited coverage:

- Ketamine therapy for severe depression receives selective coverage

- Biofeedback and neurofeedback may be covered for certain conditions

- Art and music therapy coverage varies by plan and medical necessity

- Acupuncture for mental health rarely receives coverage currently

- Meditation and mindfulness programs sometimes covered as wellness benefits

Integrated Behavioral Health Models

Progressive insurance companies promote integrated care models combining physical and mental health services. These programs improve outcomes while reducing overall healthcare costs through better care coordination.

Collaborative care models embed mental health professionals within primary care settings. Insurance reimbursement structures increasingly support these integrated approaches, recognizing their effectiveness for common conditions like depression and anxiety.

Verifying Your Mental Health Benefits

Understanding your specific coverage requires active investigation. Insurance documents use complex terminology that obscures actual benefits and limitations.

Essential Questions to Ask Your Insurer

Contact your insurance company directly to clarify mental health coverage details:

- Which mental health services require prior authorization?

- How many therapy sessions does my plan cover annually?

- What is my copayment or coinsurance for outpatient mental health visits?

- Does my plan cover psychological testing and evaluations?

- Which mental health providers are in-network in my area?

- What substance abuse treatment programs does my plan cover?

- Does my plan cover telehealth mental health appointments?

- What is the process for appealing denied mental health claims?

Document all conversations with insurance representatives including dates, times, and specific answers provided. This documentation proves valuable if coverage disputes arise later.

Reviewing Your Explanation of Benefits

After receiving mental health services, carefully review your Explanation of Benefits (EOB) statement. This document shows:

- Services provided and associated billing codes

- Amount charged by the provider

- Insurance payment and adjustment amounts

- Your financial responsibility

- Application toward deductibles and out-of-pocket maximums

Discrepancies happen frequently in mental health billing. Compare EOB statements against what your provider told you about coverage. Contact your insurer immediately if charges seem incorrect or exceed expected cost-sharing amounts.

Advocating for Better Mental Health Coverage

Despite federal parity laws, enforcement gaps and insurer practices sometimes limit mental health access. Patient advocacy improves both individual outcomes and systemic change.

Filing Parity Complaints

If you suspect your insurance company violates mental health parity requirements, file formal complaints with appropriate regulators. State insurance departments investigate parity violations for state-regulated plans. The Department of Labor oversees employer-sponsored ERISA plans.

Document specific examples showing differential treatment between mental health and medical services. Compare prior authorization requirements, visit limitations, cost-sharing structures, and network adequacy.

Working With Your Provider

Mental health professionals navigate insurance challenges daily and can advocate effectively on your behalf. They understand medical necessity criteria, authorization processes, and appeal procedures.

Request that your provider:

- Submit comprehensive prior authorization requests with detailed clinical justification

- Appeal claim denials with supporting documentation

- Provide superbills for out-of-network reimbursement if needed

- Document treatment plans emphasizing medical necessity

- Communicate directly with insurance reviewers about treatment recommendations

Collaborative advocacy between patients and providers achieves better coverage outcomes than either party working alone.

Knowing Your Appeal Rights

Every insurance denial includes appeal rights and instructions. Most plans offer multiple appeal levels before external review becomes available.

First-level appeals involve internal insurance company review by different personnel. Submit additional clinical documentation, provider letters supporting medical necessity, and relevant research supporting proposed treatment.

External review by independent medical experts becomes available after exhausting internal appeals. These reviews frequently overturn insurer denials, particularly for mental health services where medical necessity determinations involve clinical judgment.

Planning for Mental Health Care Costs

Proactive financial planning reduces stress and ensures access to needed mental health services regardless of insurance limitations.

Using Health Savings Accounts and Flexible Spending Accounts

Tax-advantaged accounts help manage mental health expenses. Health Savings Accounts (HSAs) paired with high-deductible health plans allow pre-tax savings for qualified medical expenses including mental health care.

Flexible Spending Accounts (FSAs) through employers enable pre-tax payroll deductions for anticipated healthcare costs. Mental health copayments, therapy sessions, and prescription medications qualify as eligible expenses.

Both account types reduce your effective cost for mental health services through tax savings. Maximum contribution limits change annually, so verify current limits when planning.

Payment Plans and Sliding Scale Options

Many mental health providers offer payment plans for services not fully covered by insurance. Monthly installment arrangements make comprehensive evaluations and intensive treatment programs financially accessible.

Sliding scale fees adjust costs based on income and ability to pay. Community mental health centers, university training clinics, and nonprofit organizations frequently provide sliding scale services.

Don't avoid necessary mental health care due to cost concerns. Discuss financial limitations openly with providers who can often identify affordable solutions.

Understanding health insurance for mental health empowers you to access necessary care while managing costs effectively. Federal parity laws provide strong protections, but navigating coverage details and advocating for appropriate benefits remains essential for maximizing your mental health insurance.

Whether you need ongoing therapy, comprehensive psychological evaluations, or specialized assessments, Alquimedez Mental Health Counseling provides expert services while helping you navigate insurance coverage complexities. Our team understands authorization requirements, medical necessity documentation, and effective advocacy strategies that maximize your benefits. Contact us today to discuss your mental health needs and insurance coverage options.